This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish. Cookie settingsACCEPT

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

Rebecca brings more than two decades of financial leadership, tax expertise

and operational strategy to her role. She oversees financial planning, corporate accounting, and fiscal operations across all UV&S divisions, ensuring a consistent focus on sustainability, scalability, and strategic growth.

Rebecca began her career as Tax Manager for Summerfield Hotel Corporation, where she managed corporate and partner tax filings for more than 40 properties and supported the company through its merger with Wyndham Hotels and Resorts. During the early years of raising her family, she launched a consulting practice focused on new business development and corporate taxation, helping small to mid-sized companies optimize their structures, systems, and profitability.

Her career later expanded into operations leadership, including serving as General Manager for Water’s Edge at Bluestem Communities, where she led major renovations, system upgrades, and cross-departmental process improvements. Before joining UV&S, she held the role of Vice President of Finance at Ember Hope Youthville, contributing to mission-aligned financial oversight in the nonprofit sector. Known for designing creative financial systems and solutions, Rebecca is passionate about aligning fiscal integrity with operational efficiency. Outside of work, she enjoys spending time with her family, exploring her faith, and staying active with her husband.

Dean’s career in media began at a few of the major studios, Walt Disney and

Buena Vista International, before he founded his own successful media asset company, which later became part of UV&S. Over the years, he has attended more Cannes Film Festivals and international markets than he can reliably recall, giving him a wealth of industry expertise and a deep understanding of the fast-paced world of media and events. Now, he heads all UV&S businesses in the UK, driving innovation and growth across the company.

Dan leads innovation across infrastructure, cybersecurity, & digital preservation,

supporting UV&S’s broader growth strategy with a focus on scalable, future-ready solutions.

Dan began his career in the U.S. Air Force, helping deploy some of the military’s earliest internet and telecommunications systems across Europe and Southwest Asia. He later moved into IT leadership roles in the private sector, gaining expertise in network engineering and large-scale infrastructure. He went on to found and lead a technology firm focused on enterprise IT before being acquired by UV&S in 2016.

At UV&S, Dan has led initiatives spanning secure storage, cloud systems, and digital innovation—including the launch of the company’s U.S.-based film digitization division. Outside of work, Dan enjoys travel, treasure hunting, gold prospecting, and collecting sports cards, and is an advocate for animal rights in his local community.

Brandon oversees day-to-day execution across the company’s storage,

shredding, and logistics services. Since joining the company in 2014, he has played a key role in optimizing operational performance and maintaining the standards of security and reliability UV&S is known for.

Brandon previously served as General Manager of the Shredding Division and held earlier roles in financial leadership, bringing a strategic mindset to operational execution. His experience spans facility management, compliance, customer experience, and cross-division collaboration.

He holds a master’s degree in accounting from Kansas State University and brings more than a decade of operational leadership to his role. Brandon works closely with team leaders across all of the US locations to ensure smooth execution and long-term growth.

Jeff has been the driving force behind the dramatic growth & diversification

of UV&S since joining the company in 2010. Named President in 2023, he guides the company’s strategic direction from its corporate headquarters in Hutchinson, Kansas—overseeing operations in records management, IT services, international event services, and film restoration and digitization. His approach blends vision with authenticity, helping position UV&S as a leader across multiple service sectors in both the United States and Europe, while preserving the family-run culture that has defined the company since its founding in 1959.

Before joining UV&S, Jeff held leadership positions in both nonprofit and for-profit organizations, including his role as President and CEO of the Kansas Cosmosphere and Space Center. These experiences gave him insight into leading mission-driven teams through growth and innovation. A published author, keynote speaker, and full-time daydreamer, he brings creativity and vision to every aspect of his leadership.

COMMUNITY SHRED EVENTS

Host a Secure Shred Event in Your Community

UV&S partners with local businesses and organizations to host Community Shred Events—a great way to give back, build trust, and help individuals protect themselves against identity theft. These events are open to the public or your client base and promote responsible document destruction in a secure, professional setting.

Host a Shredding Event !

Public-Facing Events with a Purpose

UV&S supplies trucks, staff, and shredding equipment

Promote identity theft prevention and awareness

Open to the public or invite-only for your clients

Designed for personal documents (no bulk/commercial loads)

Simple, branded community outreach

Available in Kansas, the KC Metro, Kentucky, and Indiana

Old equipment can expose your business to unnecessary risks. UV&S offers secure e-waste destruction services that keep your data safe and your disposal process compliant. Unlike some vendors, we never resell whole devices—every item is securely handled, destroyed, or responsibly recycled.

Junk computers to be dispose of

Protect Data While Reducing Waste

Recycling of laptops, desktops, keyboards, mice, & more

Certified Destruction for Complete Data Protection

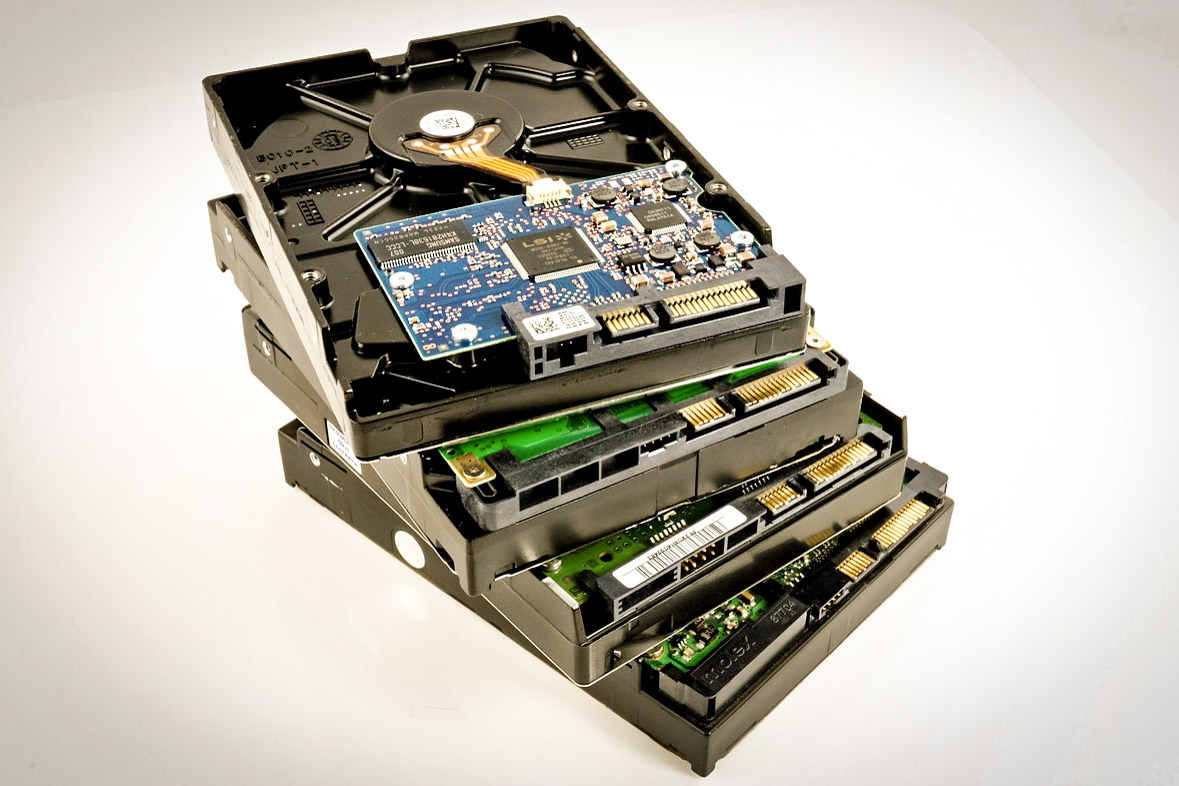

Erasing a hard drive doesn’t mean your data is gone. UV&S physically destroys hard drives ensuring data is 100% irretrievable. As a NAID AAA Certified provider, we offer destruction you can trust—whether you’re disposing of a single drive or decommissioning an entire server room.

Hard drives destruction

Secure & Compliant Data Destruction

Shredding of hard drives, and SSDs

Certificates of Destruction for every job

HIPAA, GLBA, and FACTA compliant

Chain-of-custody and serial number listing

Secure, local service across KS, MO, OK, KY, and IN

Certified Shredding for Documents and Digital Media

From paper records to old CDs and x-rays, UV&S provides secure shredding services designed to protect sensitive information and ensure compliance. Whether you need one-time document destruction or scheduled service, our NAID AAA Certified team delivers peace of mind and a complete chain of custody—on-site or off-site.

Shredded paper

Flexible Shredding Options for Every Need

Mobile or off-site shredding available

Shred paper, CDs, DVDs, flash drives, x-rays, and more

Secure containers available for scheduled pickups

NAID AAA Certified for secure document destruction

316-838-2121

707 E. 33rd St. N..

Wichita, KS 67219

US STORAGE

Secure & Specialized Storage + Shredding Across the U.S.

UV&S provides secure storage solutions across multiple U.S. locations. Our underground and above-ground facilities safeguard critical data, documents, and media with tailored environments for long-term preservation. We also offer secure shredding services to ensure the compliant destruction of sensitive records when they are no longer needed.

Storage & recycling in the U.S.

Why Choose UV&S?

Multiple secure storage locations, including underground vaults

Climate-controlled options for media, records, and data

High-security access restrictions and 24/7 monitoring

Disaster-resistant storage for ultimate protection

Secure shredding services for document disposal and compliance

Premier storage & recycling solutions in the United Kingdom

Located in Ashford, London, UV&S offers specialized storage in climate-controlled vaults and secure ambient storage. Choose from Essential Vaults, Premier Vaults, and Exclusive Vaults to protect your valuable assets. Our comprehensive recycling services ensure safe and sustainable disposal of records and media.

Storage & recycling in the U.K.

Why Choose UV&S U.K. Storage & Recycling?

Secure storage for film, media, records, and valuable assets

Climate-controlled vaults to ensure optimal preservation

Flexible storage options, including private compartments

High-security facilities with restricted access Convenient location near London with expert support

Recycling services for responsible document and media disposal

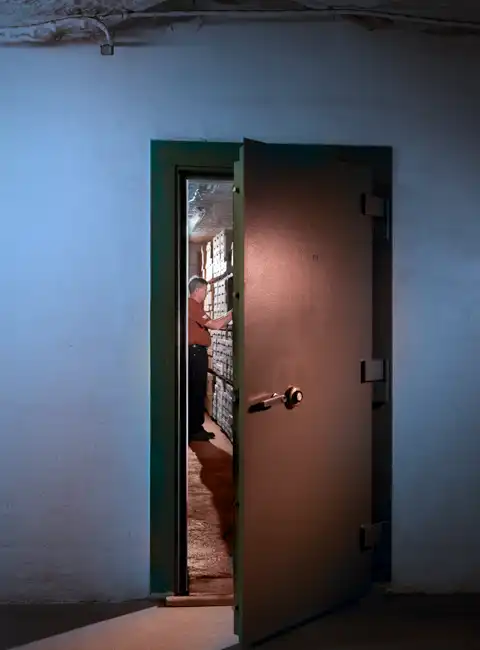

Looking for the highest level of security for your sensitive media, critical data, or important records? Our underground storage solutions offer unparalleled protection against both natural and man-made disasters, ensuring your assets are safe and secure.

Refrigeration storage

Advantages of Choosing UV&S Underground Storage:

Maximum Possible Protection – Designed to withstand various natural and man-made disasters, offering the highest level of security.

Environment Extends the Life of Your Media – Stable conditions help preserve the integrity of your materials, preventing deterioration over time.

Flexible and Customizable to Your Needs – Whether you need specific climate controls or unique security features, our underground storage can be customized to fit your exact requirements.

Fast Client Access – Despite being secure, our facilities allow for fast and easy access to your materials when needed.

Private Vault Storage – Maximum Security and Customization

Certain materials demand precise temperature and humidity control to prevent degradation. Our refrigerated and climate-controlled storage solutions maintain a cool, dry environment designed to extend the life of film elements, sound recordings, microfilm, and other delicate media. For specialized needs, we offer customizable vaults with advanced security measures.

Refrigeration storage

Essential Features for Long-Term Preservation

Custom Vaults & Private Compartments – Secure, dedicated storage spaces tailored to your needs

Stable Climate Control – Consistent temperature and humidity to prevent deterioration

Disaster-Resistant Protection – Underground storage safeguards against natural disasters, civil unrest, and other risks

When flat media and delicate records require secure, space-efficient storage, our drawer storage solutions provide the perfect fit. Designed for engineering documents, architectural plans, artwork, historical records, and microforms, our environmentally controlled facilities ensure long-term preservation and easy access.

Drawer storage solutions

Optimized Storage for Archival & Technical Document

High-Density, Space-Saving Solutions – Organized cabinets to maximize storage efficiency

Controlled Storage Environment – Stable temperature and humidity for long-term media preservation

Disaster-Resistant Protection – Underground facilities offer natural security against fire, water, and other threats

Flexible Storage Options – Choose from our selection of cabinets or request a custom order

Expert Customer Service – Our team ensures quick retrieval and exceptional support

Private Vault Storage – Maximum Security and Customization

Looking for exclusive, high-security storage designed to meet your exact needs? Our private vaults provide dedicated, fully customizable space for confidential records, artifacts, and high-value assets. Unlike shared storage options, your space is yours alone, ensuring maximum separation, security, and control.

Private Vaults Storage

Your Secure Space, Your Specifications

Customizable Storage Solutions – From 100 sq. ft. micro vaults to 15,000 sq. ft. private facilities

Maximum Security Options – Further access restrictions, reinforced protection, and private entry

Underground, Disaster-Resistant Locations – Natural protection against environmental threats

Exclusive Access & Privacy – Your vault can be completely separate from other stored assets

Secure Storage for Confidential Documents & High-Value Items

Unmatched Customer Service – A responsive, expert team to meet your needs

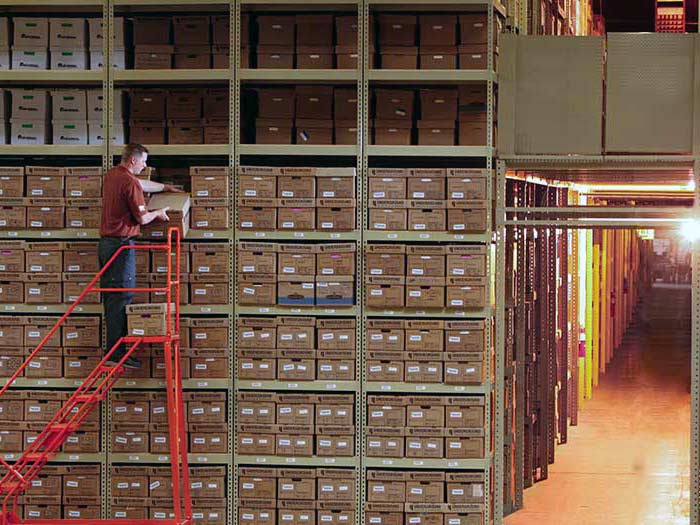

Running out of space? Protect your critical records while reducing costs with UV&S offsite box storage. Our secure facilities keep your documents organized, accessible, and safe from damage, theft, or loss. Whether you need to store a few boxes or thousands, we provide scalable solutions with a personalized, responsive approach you won’t find with other storage companies.

Archive Storage Solutions

Why Choose UV&S Box Storage?

Cost-Effective & Secure – Free up office space and reduce storage expenses

Barcode Tracking & Inventory Management – Know exactly where your records are at all times

Fast, 24/7 Access & Retrieval

Get the documents you need when you need them

Expert Handling & Transport – Safe racking, retrieval, and transportation services available

Flexible Storage for Any Volume – From a few boxes to entire archives; point forward or transfer all records to us

Exceptional Customer Service – A responsive team that truly cares about your storage needs

Your files are your future, whether it’s today’s spreadsheet, last year’s box of documents or a data tape from 30 years ago. Since 1959, UV&S has grown to be a world leader in secure storage. Organizations of all sizes entrust UV&S with their most prized assets, from movie studios to manufacturers, financial firms to family businesses. When it absolutely has to be safe off-site storage is the key to protecting your assets.

Bad things can happen to good companies: Weather damage, water leaks, break-ins, electrical fires and worse. Our nationwide facilities offer you maximum protection from disaster, deterioration and theft.

Whether they’re located in one of our aboveground or underground facilities, your assets are in a well-protected, climate- controlled area that prevents unauthorized access. We offer unlimited, secure storage space that can be customized to meet your privacy and furnishing needs. Thousands of companies worldwide trust UV&S to protect their vital assets.

OUR SMALL BUSINESS SERVICES INCLUDE:

Complete records and information management: We offer 24/7 access and fast, affordable storage, retrieval and delivery of your important records.

Storage consulting: Call us for disaster planning, records organization, business impact analysis and more.

Data tape rotation: Set your schedule, and we’ll safely transport your data to and from our many vaults.

Destruction and shredding: Certified, bonded destruction of sensitive documents.

Micrographic services: Climate-controlled storage, management and tracking, imaging, preservation and more.

Document conversion: Transfer paper documents to digital media for fast access.

Data security services: Ensure the safety of your critical data with UV&S co-location and backup.

Dedicated transportation fleet: Guaranteed secure delivery to and from our location to yours.

Special projects: From indexing and inventory, to fulfillment services to imaging projects, we can help.

The oil and gas industry has come a long way since we first began storing geological maps in the early 1960’s. Core samples, well logs, seismic data tapes; we store it all for some of the biggest energy companies in the world.

Oil and gas records are more like assets than records – tremendously valuable to exploration and production. Seismic maps are data intensive, requiring massive amounts of storage.

UV&S offers three unique facilities for seismic data libraries, support data, business records, maps, and core samples. We offer same day retrieval, same day shipping, and a wholly-owned transportation fleet to meet your needs for fast, secure access.

Every year, news reports detail instances of natural disasters, substandard storage conditions, fire, theft and vandalism. Much of the nation’s collection of art and artifacts rots in humid basements or hot warehouses, waiting for a pipe to burst. Entire collections of art, artifacts, and documents are lost or damaged.

For more than 50 years, national museums and private collectors alike have trusted UV&S for the protection of their cultural treasures. Our natural underground atmosphere keeps your items cool and dry and bar-coding and inventory technology ensure constant tracking.

At UV&S, we have more than 50 years experience storing and managing vital medical records. From patient records and data tapes to oversized x-rays and more, you can relax knowing your records are safe from the elements, filed away for easy retrieval and secure in our vault 650 feet underground.

Off-site healthcare records storage offers additional efficiencies, enhanced security, and eased HIPAA compliance. Reduce storage costs, boost compliance, protect patient information and prevent electronic records loss with UV&S.

We help you manage your records throughout their complete lifecycle. From the time we take possession of the files at your practice until their eventual destruction, your files never leave our possession — no third party transportation companies, no sending them through the mail. We handle legal and industry specific compliance concerns and you maintain 24/7 access with digital file transfer and a dedicated transportation fleet.

Your business is to hedge against potential future loss. Our job is to protect your records and data from loss due to natural disaster, man-made disaster, theft and improper storage conditions.

Insurance companies understandably generate a large volume of paper records and electronic data. Actuarial statistics and probability analysis are data intensive and must be preserved. Client contracts, riders, medical information, forms and payment information are subject to privacy concerns and industry legislation. They must be protected in a way that limits legal exposure and provides efficient access.

UV&S can help you meet your insurance records storage and compliance needs.

Court records storage has become a specialty for UV&S. City, county, parish, state and federal departments and agencies from across the nation rely on UV&S for security, efficient records management, and preservation. Whether you are a County Clerk, a Register of Deeds, a Registrar of Voters, or a Chief Information Officer – we can help you balance the needs for compliance, public information access, and private information protection.

Court clients include courthouses, district courts, probate courts, juvenile courts, public defender offices and district attorney offices.

Court records stored at any of our facilities are as accessible as they would be in your own jurisdiction or district – they can be faxed, scanned and digitally transferred, shipped overnight, or transported by our wholly-owned fleet of vehicles. Clerks of Court from across the nation rely on us to provide economical and secure storage.

A familiar phrase within the film and television industry, Send it to the Salt Mine has come to stand for incomparably secure and remarkably affordable film and sound archiving.

Going underground began decades ago. Film and television studios recognized that our uniquely cool and dry atmosphere, the distance from natural disaster and metropolitan exposure, and our location 58 floors below ground, were ideal for long term archiving of movie films. We eliminated high warehouse lease rates as well as reduced labor and utility costs. Our film vaults are void of anything that challenges asset protection at surface level, including seismic activity, fires, and intrusion.

We are recognized as a leader in secure storage for the motion picture and entertainment industry and have multiple locations that offer climate controlled vaults, refrigerated storage, bonded inspection and cataloging services, same day retrieval, same day shipping, and refrigerated transportation services.

UV&S is a proud member of the Association of Moving Image Archivists (AMIA).

Secure bank records management is essential to meeting your auditor and customer demands. Industry legislation, such as Gramm-Leach-Bliley ACT (GLB), the Sarbanes-Oxley Act (SOX) and the Fair and Accurate Credit and Transactions Act (FACTA), combined with government regulation and oversight, create the need for a rigorous bank records management program that addresses securing private information, storing records according to an acceptable retention schedule and destroying information that has passed its retention date.

At UV&S, we have served Fortune 500 companies and small community banks alike, since 1959. Our experienced staff, secure facilities and time-tested procedures are ready to help you meet those demands.

Not all media vaults are the same. Is your data stored in a controlled, secure environment? We provide climate-controlled, high-security media vaults—both underground and above ground—to safeguard your data from theft, disasters, and tape degradation. Whether you need permanent tape storage or active rotations, our facilities ensure fast access and long-term protection.

Media Vaults Storage

Comprehensive Tape & Archive Storage Solutions

Tape Vaulting & Rotation Services – Secure offsite storage for backup tapes, ensuring quick retrieval and reliable data protection

Library Storage – Barcoded and organized for efficient cataloging and retrieval of large data volumes

Legacy Archiving – Cost-effective storage for outdated media, including open-reel tapes and other legacy formats

Disaster Recovery-Ready – Protection from natural and manmade threats

24/7 Monitored Climate Control – Temperature and humidity regulated to industry standards

Geographic Separation – Reduce risk with offsite storage

UV&S has multiple climate-controlled vault options, including Essential Vaults, Premier Vaults, and Exclusive Vaults, along with Ambient storage in the United Kingdom.